By: Governor Lael Brainard

At the Urban Institute, Washington, D.C.

Good morning. I am pleased to be here at the Urban Institute to discuss how to strengthen the Community Reinvestment Act (CRA), which is a key priority for the Federal Reserve. The CRA plays a vital role in bringing banks together with community members, small businesses, local officials, and community groups to make investments in their community’s future.1 That is why we are committed to getting CRA reform done right.

The Origins and Purpose of the CRA

Any successful reform must be grounded in the origins of the CRA and its ongoing importance to low- and moderate-income (LMI) neighborhoods. The CRA was one of several landmark pieces of legislation enacted in the wake of the civil rights movement intended to address inequities in the credit markets. By passing the CRA, Congress aimed to reverse the disinvestment associated with years of government policies and market actions that deprived lower-income areas of credit by redlining—using red-inked lines to separate neighborhoods deemed too risky.2 By conferring an affirmative and continuing obligation on banks to help meet the credit needs in all of the neighborhoods they serve, the CRA has not only prompted banks to be more active lenders in LMI areas, but also important participants in multisector efforts to revitalize communities across the country.

Pursuant to guidance from the Board of Governors, each of our Federal Reserve Banks houses a group of dedicated community development professionals and CRA examiners to help banks meet their CRA obligations. We are proud of our work in familiarizing banks with the CRA’s provisions, introducing banks to potential partners in their communities, and convening conferences to disseminate research and best practices.3

The CRA plays a vital role in the ecosystem supporting economic opportunity in LMI communities in both rural and urban areas. Rather than direct funds to specific projects, the CRA encourages banks to engage on the priorities identified by local leaders and more broadly serve credit needs of small businesses and residents of these communities. By being inclusive in their lending and investing, banks help their local communities to thrive, which in turn benefits their core business. The recognition of this mutually beneficial relationship between banks and their local communities is one of the core strengths of the CRA and the reason our effort to revise the CRA regulations must focus on local needs and stakeholder input.

What Have We Learned from Stakeholders?

For several years, the federal banking regulators have been asking stakeholders for input on strengthening the CRA regulations to help banks better meet the credit needs of the local LMI communities they serve and more closely align with changes in the ways financial products and services are delivered. We also have heard calls from banking and community organizations for the use of metrics to provide greater upfront clarity about evaluation standards. We have heard that branches remain as important as ever to their local communities, even as the growth of mobile and online services has extended the geographic area that banks are serving.4 The one message we have heard most consistently is that banks and community organizations alike value the activities they undertake under the auspices of the CRA and have invested considerable time and effort in the associated processes and reporting.5 For that reason, stakeholders have asked the regulators to take care as we contemplate changes to the CRA.6

If the past is any guide, major updates to the CRA regulations happen once every few decades. So it is much more important to get reform right than to do it quickly. If we only have one opportunity for a few decades, I want to make sure CRA reform is based on the best analysis and ideas and the broadest input available. It is critical to analyze carefully the likely effects of any proposed changes on credit access and community development in LMI communities, as well as any additional reporting and procedural burdens for banks.

Last year, we set out several principles to guide our work on CRA reform.7 Revisions to the CRA regulations should reflect the credit needs of local communities and work consistently through the business cycle. They should be tailored to banks of different sizes and business strategies. They should provide greater clarity in advance about how activities will be evaluated. They should encourage banks to seek opportunities in distressed and underserved areas. And they should recognize that the CRA is one of several related laws to promote an inclusive financial sector.

Grounding Metrics in Analysis Based on Data

Guided by stakeholder input, we evaluated how to strengthen the regulation by using metrics to provide greater certainty about how activities will be evaluated, while remaining faithful to the core purpose of the CRA to make credit and retail banking services available in local LMI communities. Proposed changes to the CRA regulation must be grounded in analysis and data to avoid unintended consequences.

Because consistent data on CRA-eligible activity were not readily available, our research staff set about creating a database based on over 6,000 written public CRA evaluations from a sample of some 3,700 banks of varying asset sizes, business models, geographic areas, and bank regulators.8 The database includes the location, number, and amount of CRA-eligible loans and investments and the ratings associated with each bank’s performance. The data go back to 2005 in order to assess how CRA performance and the associated ratings vary across the economic cycle.

Metrics that Make Sense

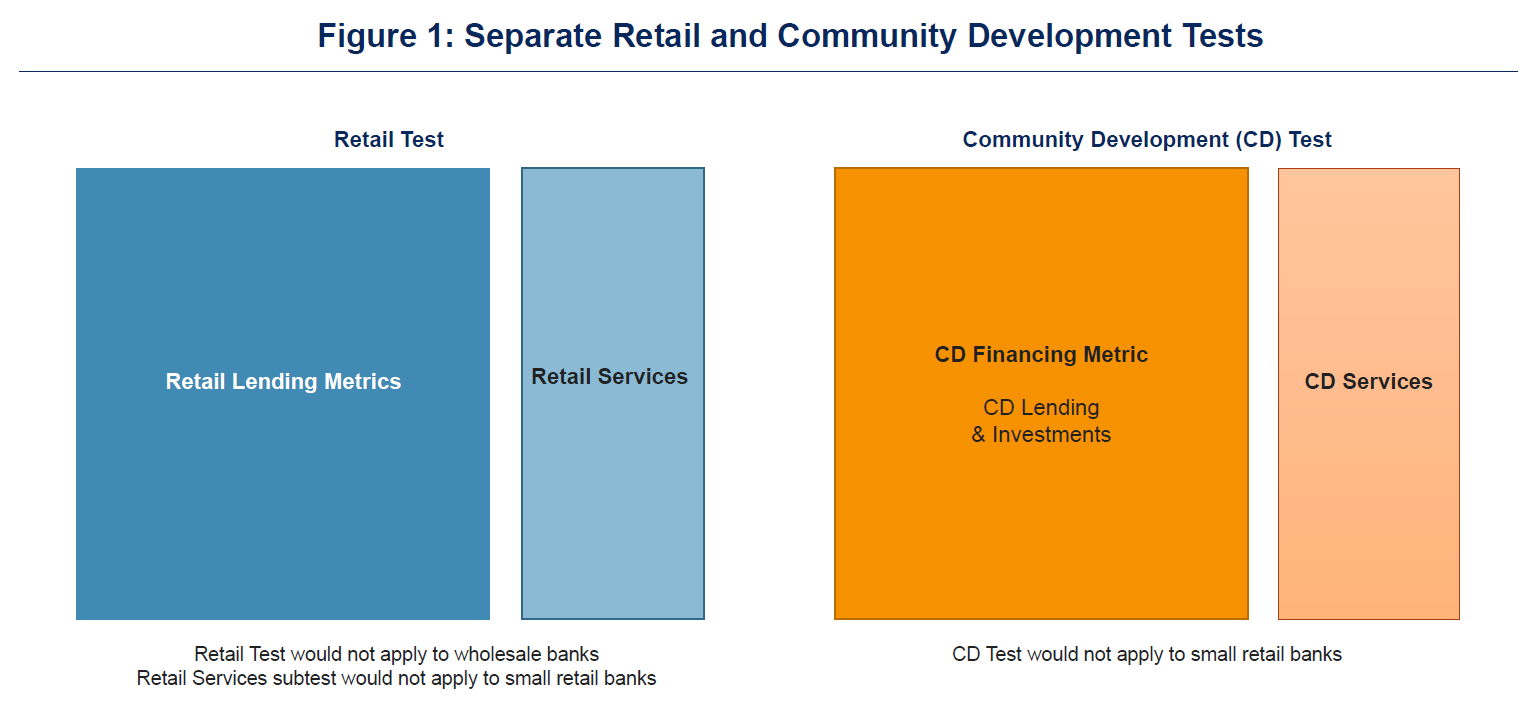

So how can we use metrics to provide greater clarity about evaluations? I will sketch out a proposed approach that uses a set of tailored thresholds that are calibrated for local conditions. It starts by creating two tests: a retail test and community development test (figure 1). Broadly speaking, all retail banks would be evaluated under a retail test, which would assess a bank’s record of providing retail loans and retail banking services in its assessment areas. Large banks, as well as wholesale and limited-purpose banks, would also be evaluated under a separate community development test that would evaluate a bank’s record of providing community development loans, qualified investments, and services.

{kind=link}

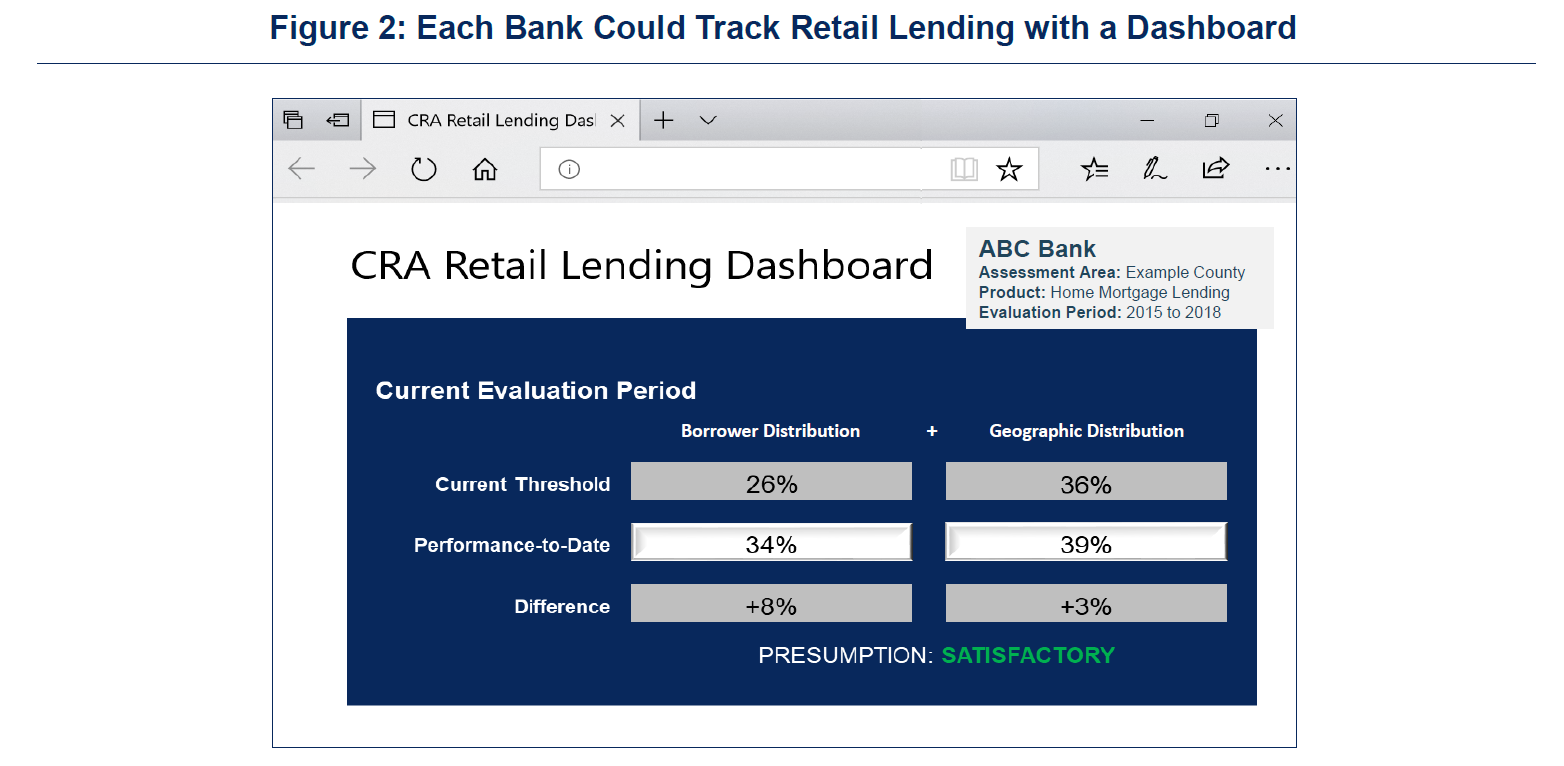

Using bank and other publicly available data, we would be able to provide a bank with a dashboard indicating how its retail lending activity compares to thresholds for presumptive satisfactory performance that reflect the activity of other lenders and credit demand in the local area. Separate metrics reflecting a bank’s assessment area can be provided related to the evaluation of its community development performance.

Dividing evaluations into separate retail and community development tests is important. First, evaluating all retail banks under a stand-alone retail test is important to stay true to the CRA’s core focus on providing credit in underserved communities in an assessment area. In contrast, an approach that combines all activity together runs the risk of encouraging some institutions to meet expectations primarily through a few large community development loans or investments rather than meeting local needs.

Second, having separate tests ensures that expectations are tailored for banks of different sizes and business models. Only larger banks would be expected to meet the community development test along with the full retail test. Similar to today, smaller banks would have the option of having their retail banking services and community development activities evaluated in order to achieve an “Outstanding” rating, but it would not be required. Moreover, small banks below some threshold might have the option to be evaluated under the existing methodology.

Third, separate retail and community development tests provide greater scope to calibrate the evaluation metrics to the opportunities available in the market, which can differ for retail lending and community development financing.

After analyzing ways to use metrics across the board, we concluded that the value of retail services and community development services to a local community do not lend themselves easily to a monetary value metric comparable to the monetary value of loans and investments. The value of these services may vary greatly from community to community. It is difficult to monetize this value in a consistent way relative to the value of lending and investment, thus introducing the risk of skewing incentives inadvertently. For example, the services and leadership provided by a small bank located in a rural community may be vital to the success of that community, even if the dollar value of those services is small compared with a branch in a large city. Because of this concern, we are inclined to propose a set of qualitative standards to evaluate retail services within the retail test, and a separate set of qualitative standards to assess community development services within the community development test.

Retail Test—Metrics for Retail Lending

The core of the retail lending test would be to use widely available data to assess two clear objectives: how well a bank is serving LMI borrowers, small businesses, and small farms in its assessment area, and how well a bank is serving LMI neighborhoods in its assessment area. The metrics used to evaluate these two questions would rely on loan counts rather than dollar value in order to avoid inadvertent biases in favor of fewer, higher-dollar value loans.9 The metrics would be evaluated separately for each major product line in a bank’s assessment area, which is important to tailor the use of metrics to a bank’s business model.

The proposed approach measures a bank’s performance in serving the needs of both low- and moderate-income borrowers (and small businesses and small farms) and LMI places in the community. For mortgage loans, an LMI borrower distribution metric would calculate the percentage of a bank’s number of loans made to LMI borrowers relative to its overall mortgage originations, and assess this percentage against an assessment area threshold determined by local demographics and the aggregate lending of other in-market competitors. A separate LMI neighborhood distribution metric would evaluate the percentage of a bank’s number of loans in LMI tracts to its overall loan count and assess this against a threshold determined by local demographics and the aggregate lending of other in-market competitors.

A bank that meets or exceeds both the LMI borrower and LMI neighborhood thresholds for each of its major product lines would be presumed to have a satisfactory-or-better level of retail lending performance in that assessment area. Using a customized dashboard, each bank could track its own activity against the threshold on an ongoing basis reflecting recent data, eliminating the lengthy uncertainty associated with the current evaluation methodology, which many banks have highlighted as the most important area for reform (figure 2).

{kind=link}

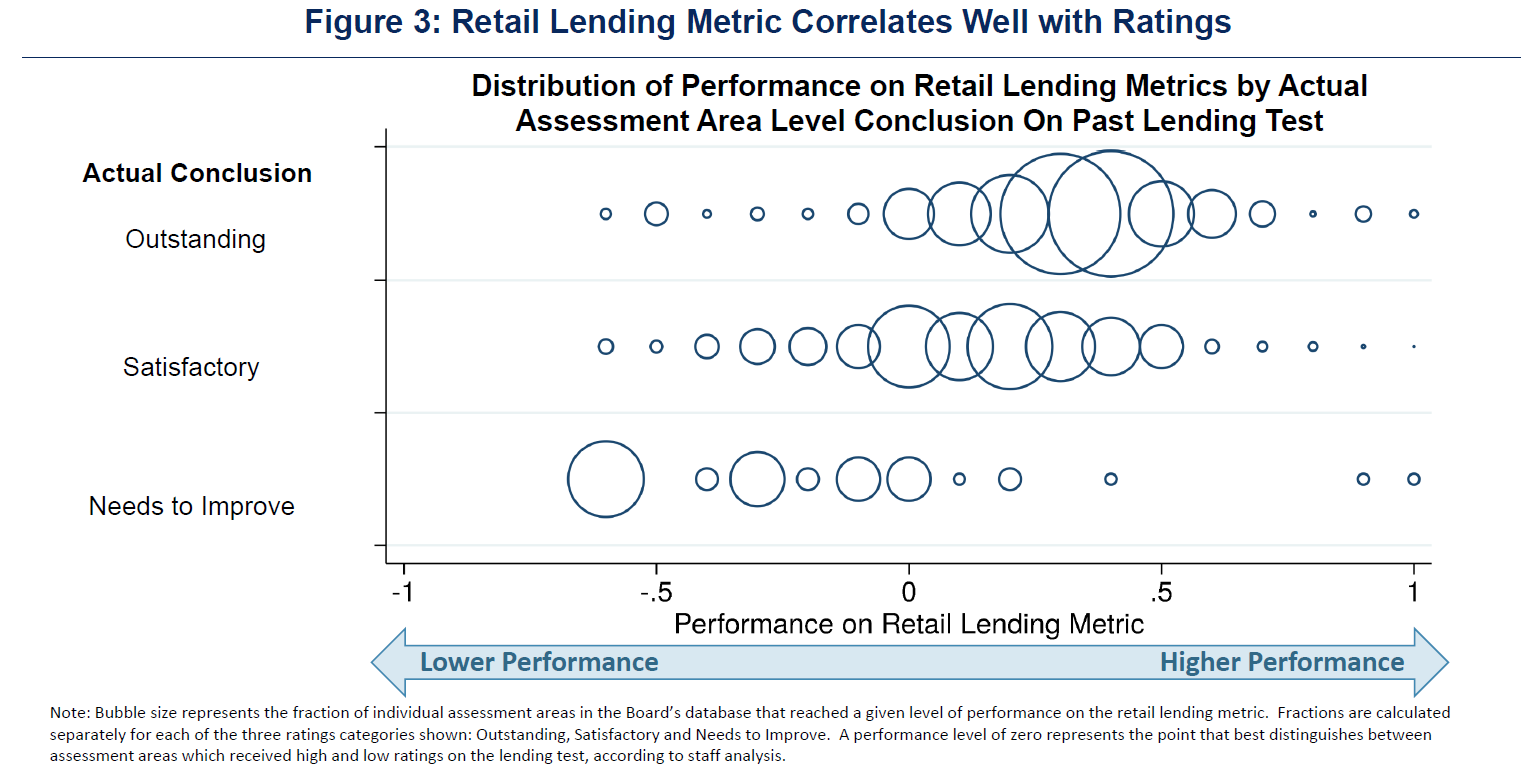

Importantly, the CRA database we have constructed confirms that the proposed retail lending metrics correlate well with past ratings of bank performance (figure 3). The specific thresholds that would establish a presumption of satisfactory performance could be informed by current evaluation procedures but need not be set at the same level, and public input will be important.

{kind=link}

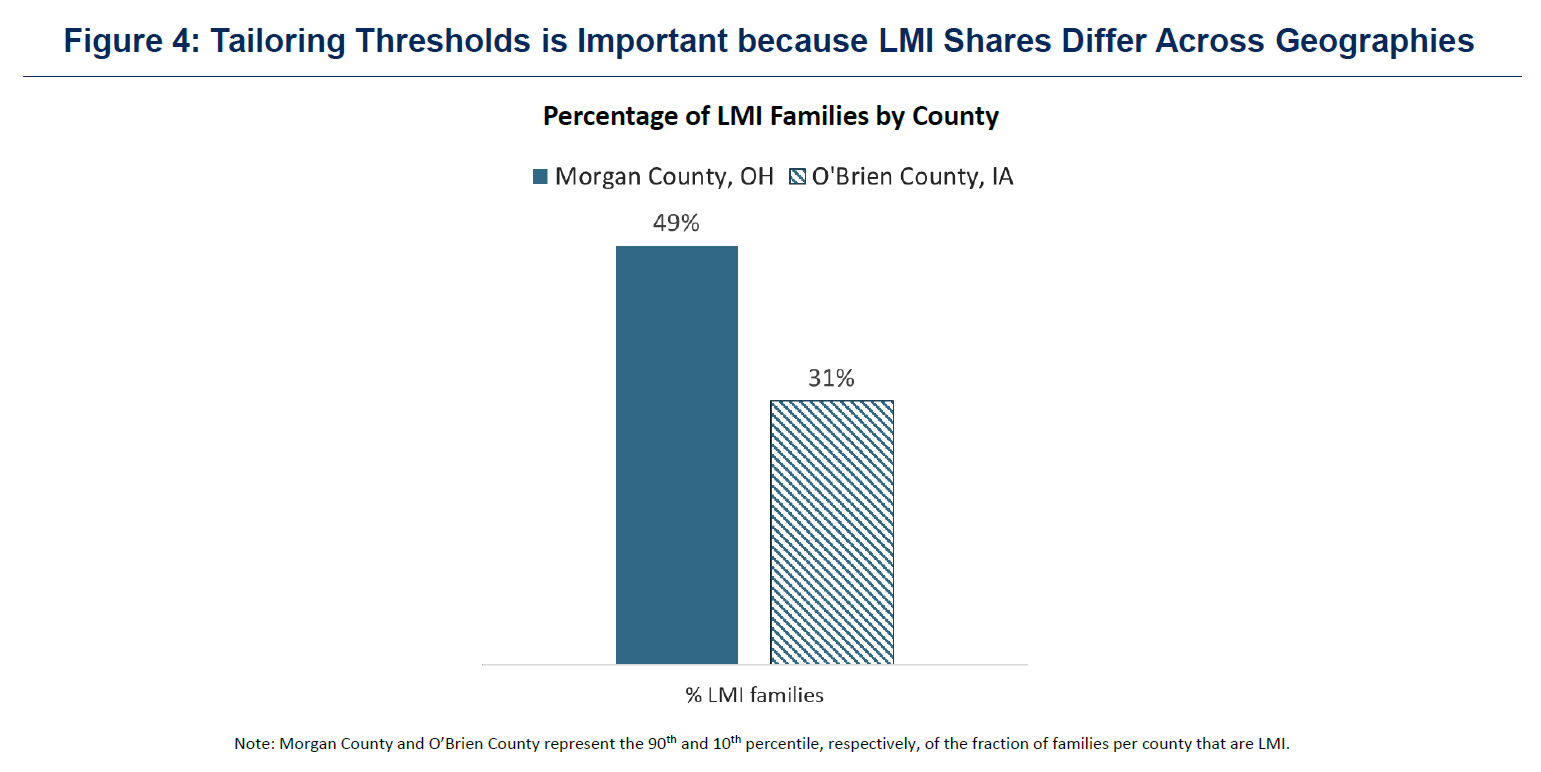

The retail lending metrics would be tailored to the needs of the local community. This tailoring is not possible with a uniform benchmark that applies to all banks and all communities. The large differences between assessment areas illustrate the importance of tailoring thresholds. For example, in Morgan County, Ohio, LMI families are 49 percent of the population, compared with 31 percent in O’Brien County, Iowa (figure 4). We believe this tailored approach is empirically sound and avoids imposing arbitrary CRA performance measures on a bank and its community. In order to ensure it meets standards of safety and soundness, CRA lending must be evaluated in the context of the characteristics of the bank and its community.

{kind=link}

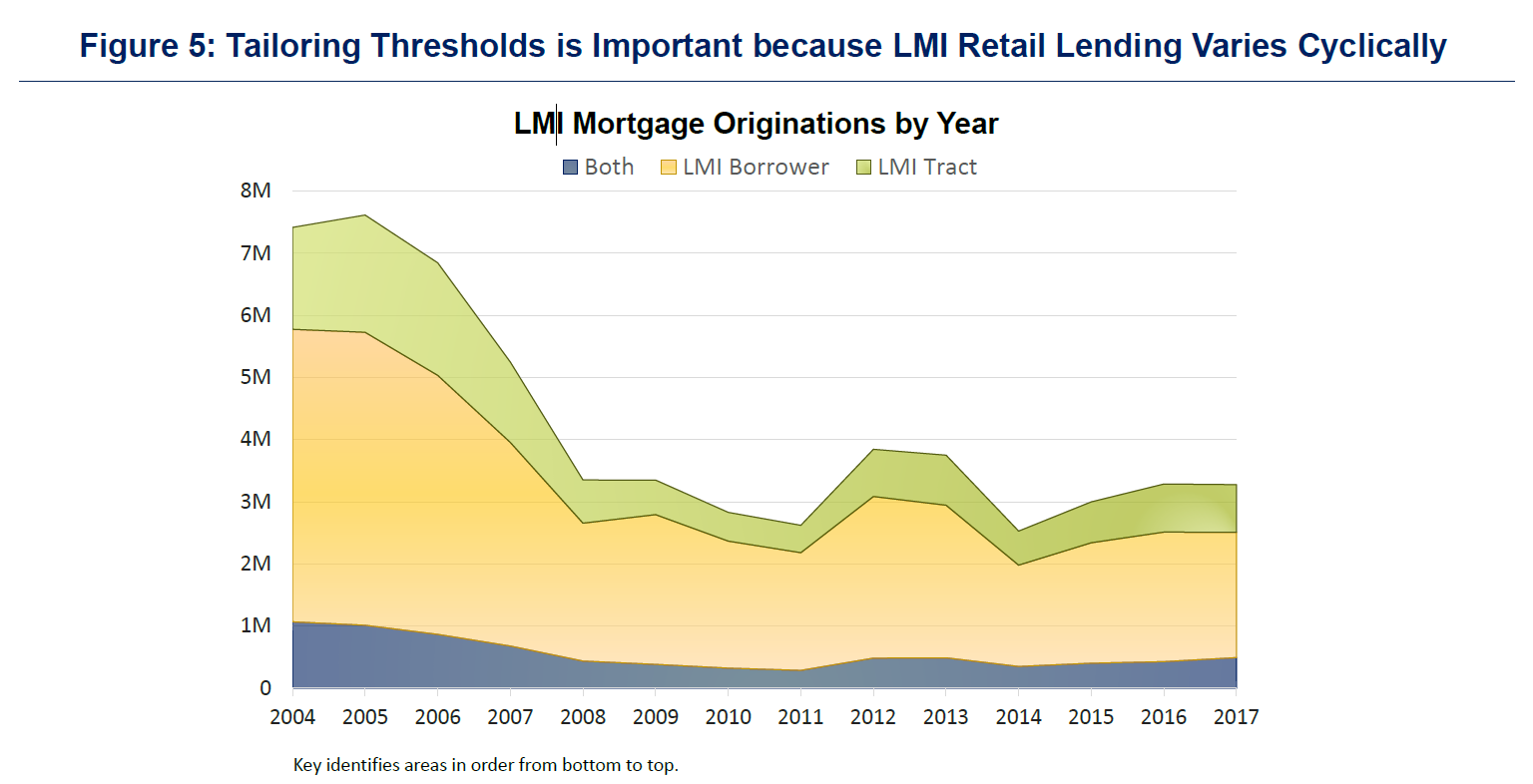

Additionally, the proposed retail lending metric would automatically adjust to changes in the business cycle. As many commenters noted in response to the ANPR, a uniform ratio that does not adjust with the local business cycle could provide too little incentive to make good loans during an expansion and incentives to make unsound loans during a downturn, which could be inconsistent with the safe and sound practices mandated by the CRA statute. Industry commenters also expressed concern that discretionary adjustments to the uniform metric are likely to lag behind the economic cycle and undermine the certainty a metric purports to provide. By contrast, the proposed retail lending metrics are calibrated to contemporaneous changes in market conditions, thereby reducing the risk of providing unsound incentives (figure 5).

{kind=link}

Finally, the proposed approach would continue to recognize local context in assessing a bank’s CRA performance. If a bank receives the presumption of satisfactory by meeting or exceeding the thresholds, an examiner could consider performance context information, including the bank’s responsiveness to the community’s needs, in determining whether the bank’s performance is outstanding at the assessment area level. Likewise, if a bank does not meet or exceed the thresholds, it would undergo a full examination, as it would currently, and could receive any level of rating, including possibly Outstanding, based on the full range of performance context considerations and clear qualitative criteria. The metrics would be designed to provide greater certainty, while avoiding rigidity.

Retail Test—Evaluating Retail Services

Retail services can be extremely important to LMI communities, although they do not easily lend themselves to consistent, comparable metrics. It makes sense to use qualitative criteria related to the responsiveness of a bank’s products and services and its delivery systems, which stakeholders highlighted as being particularly important in LMI areas.

In terms of delivery systems, we recognize the unique and important role that branches play in providing essential financial services to customers, particularly in underserved areas. Banks would be evaluated on their branch and ATM locations and how well they serve customers using online and mobile access channels. Providing a meaningful evaluation of all customer access channels is essential to ensuring that the CRA remains relevant as more banks adopt digital technology.

Recognizing that branches are important community assets, the proposed retail service test would compare a bank’s distribution of branches, including any openings or closures, to broader patterns of activity in the region. A recent report on branch access in rural areas found that just over 40 percent of rural counties lost bank branches between 2012 and 2017, with 39 rural communities being “deeply affected” by the loss of more than half of their bank branches.10 In addition to the challenges associated with higher cost and less convenient access to banking services, community leaders described how branch closures diminished their access to important leadership from branch personnel that was important to their community’s success.

Community Development Test—Measuring Lending and Investment

Next, let’s turn to the community development test for large retail banks, as well as wholesale and limited-purpose banks. The establishment of a separate community development test reflects stakeholder feedback emphasizing that the value of community development finance is distinct and not directly comparable to retail activity. A separate test also allows for a broader area to be taken into account for purposes of community development relative to retail lending.

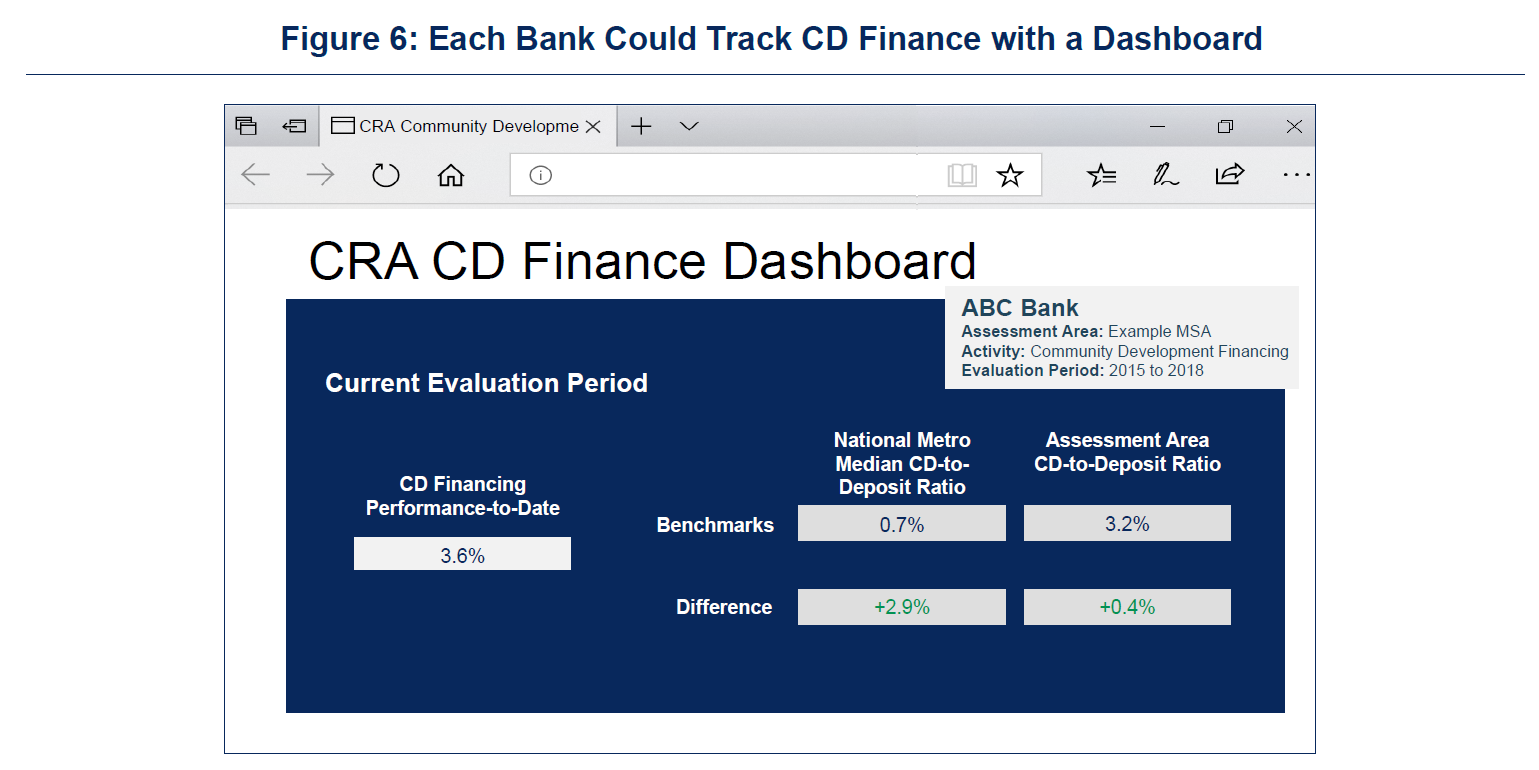

Our analysis suggests there are a set of metrics that can be compared to appropriately tailored benchmarks to provide greater certainty regarding community development lending and investment. The proposed metric would aggregate loan and investment dollars that are originated or purchased during the evaluation period with the book value of all other community development loans and investments that are held on the bank’s balance sheet (figure 6). Reflecting input from banks and community organizations that patient, committed funding has the greatest effect, this approach avoids the incentives under current practice to provide financing in the form of short-term renewable loans in order to receive CRA credit.11

{kind=link}

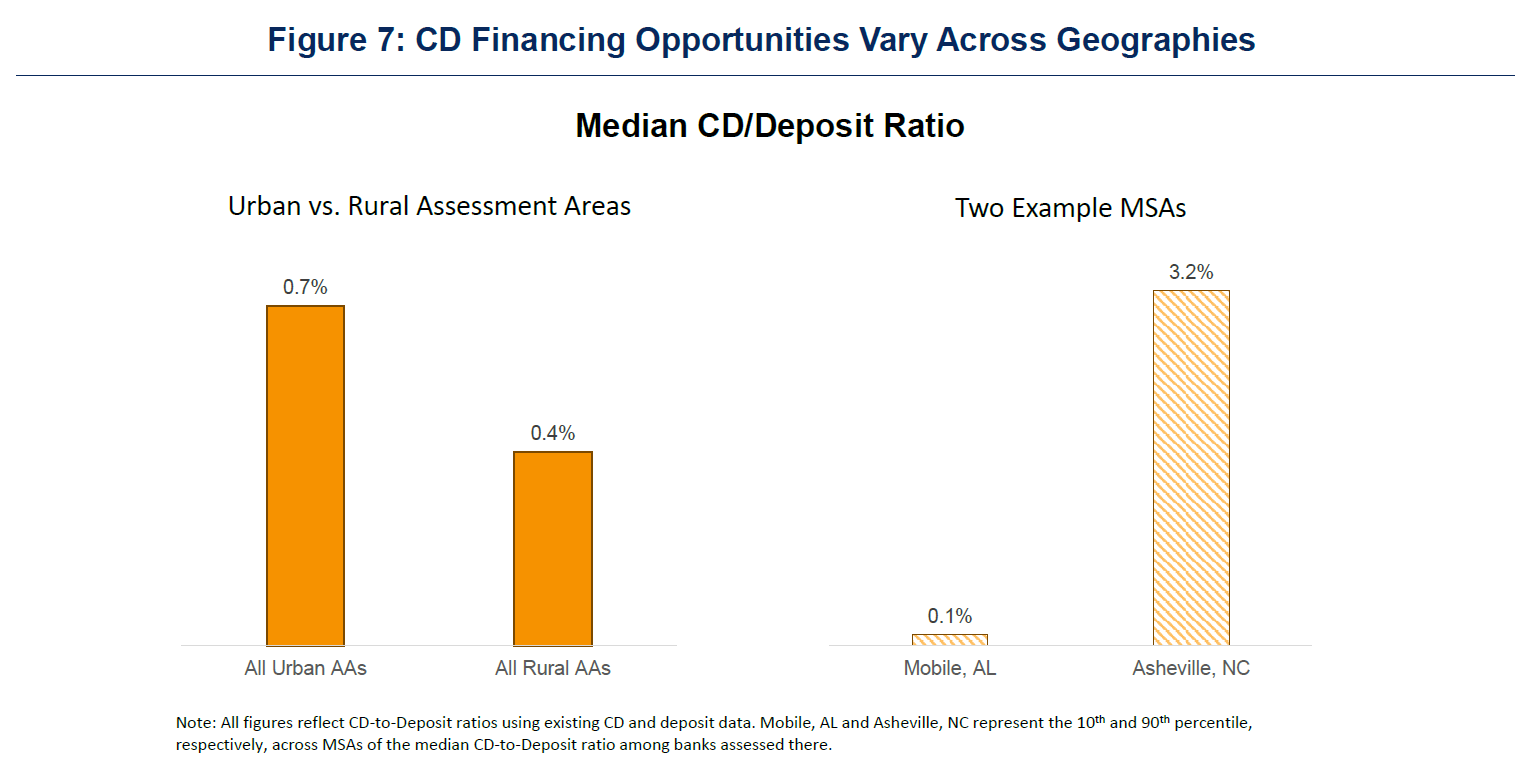

The proposed test would compare the combined measure of a bank’s community development financing relative to deposits in its local assessment area to a national average, set differently for rural and urban areas, and a local average in the bank’s assessment area. The national comparator would be set differently for metropolitan statistical areas and rural areas to reflect the comparatively lower average levels of financial infrastructure in rural communities (figure 7). The use of a national rural/metro comparator in addition to an assessment area comparator is intended to avoid skewing incentives toward financially dense areas that are already hotly competitive and to reflect the value of community development in underserved areas. The use of these comparators would help provide consistency across evaluations and clarity regarding community development expectations for both banks and communities.

{kind=link}

It is also important to recognize that community development financing is often provided in areas that do not neatly fit within a bank’s assessment area. Community development financing opportunities are not always easy for banks to identify and often depend on working with local nonprofits or governments to help identify projects and put together the complex financing required to bring them to fruition. Stakeholder feedback emphasized banks’ unique advantages in evaluating community development projects in the states and territories where they operate and providing the smaller-scale, more complex, and often more impactful, investments overlooked by institutional investors. For this reason, and to encourage more activity in underserved areas, it makes sense to give consideration to all of a bank’s community development activities in a state or territory where it has an assessment area.12

Banks want to know in advance that they will get the benefit of CRA consideration in order to invest the time and effort necessary to evaluate and structure community development loans and investments. For that reason, we are sympathetic to requests for a timely process by which banks can seek conditional examiner review of particular activities before making financial commitments, particularly for activities that revitalize and stabilize targeted areas.

Our analysis suggests a community development finance metric along the lines outlined here will help to ensure greater predictability and consistency in achieving a Satisfactory rating. However, we also want to make sure that these metrics are supplemented with clear, qualitative standards to ensure that small-scale, high-impact community development activities are rewarded, along with a bank’s responsiveness to local needs and priorities.

Community Development Test—Evaluating Services

It is also important to evaluate services qualitatively at the assessment-area level as part of the overall community development test. Volunteer and other services provided by banks can provide meaningful support to communities whose value is unlikely to be adequately captured on a comparable basis using aggregative dollar value metrics. In areas with a low density of financial services, a bank officer on the board of local community organizations could provide considerable value to the community that is not accurately reflected by monetizing volunteer hours based on their compensation.

Tailoring

This approach to assessing CRA performance would tailor performance metrics to bank size and business strategy, as well as to local and cyclical conditions. The approach would tailor to banks’ business models by establishing separate thresholds for substantially different lending products, such as mortgage loans and small business, small farm, and consumer loans, as well as separate retail lending and community development financing metrics.

The proposed metrics would also be tailored for different bank sizes. This is facilitated in part by allowing very small banks to retain the current evaluation procedures and in part by creating a separate community development test that would apply only to large banks. Tailoring is also an important consideration in data collection and reporting requirements. The proposed retail lending approach is designed so that it can be implemented in significant part with data that are readily available. In designing the community development approach, we have been mindful of burden as we consider any additional data that might be required to implement certain metrics.

Finally, as previously noted, the metrics are tailored for local conditions and cyclical considerations. The proposed threshold for each type of activity is calibrated to local conditions as they evolve over the cycle, and the community development finance metric uses an additional time-varying national rural or urban comparator.

The Path Ahead

Staff across the Federal Reserve System have devoted substantial time and effort to engaging with the other banking agencies in the CRA reform process. The analysis, data, and proposals I have discussed today have all been shared in greater detail with our counterparts at the other banking agencies in an effort to forge a common approach. We were hopeful our proposed approach could be incorporated into the proposed rulemaking that was released last month in order to seek public comment on a range of options.

Based on the best available data, we concluded that CRA metrics tailored to local conditions and the different sizes and business models of banks would best serve the credit needs of the communities that are at the heart of the statute. This tailored approach using targeted metrics also yielded more consistent and predictable overall ratings than any comprehensive uniform metric. Our analysis did not find a consistent relationship between CRA ratings and a uniform comprehensive ratio that adds together all of a bank’s CRA-eligible activities in an area. Moreover, we want to be attentive to possible unintended consequences: Because a uniform comprehensive ratio would not reflect local conditions, which can vary greatly between communities and over the cycle, a bank could exert the same amount of effort in different areas or different points in the economic cycle with very different outcomes.

We continue to believe that a strong common set of interagency standards is the best outcome. By sharing our work publicly, we hope to solicit public input on a broader set of options for reform and find a way toward interagency agreement on the best approach. The process of sharing the data and analysis informing regulatory proposals and seeking public feedback on them is critical to the regulatory process. Given that reforms to the CRA regulations are likely to set expectations for a few decades, it is more important to get the reforms done right than to do them quickly. That requires giving external stakeholders sufficient time and analysis to provide meaningful feedback on a range of options for modernizing the regulations.

I will conclude by noting that the high level of engagement and commitment on the part of banks, community organizations, and other important stakeholders give me confidence that we will succeed in strengthening the CRA’s core purpose of helping banks affirmatively meet the credit needs of their local LMI communities.

1. I want to express my appreciation to Carrie Johnson and Theresa Stark for assistance in preparing this text and to Theresa Stark for her dedication to strengthening the CRA throughout her service at the Federal Reserve Board. The remarks represent my own views, which do not necessarily represent those of the Federal Reserve Board. Return to text

2. See Richard Rothstein, The Color of Law: The Forgotten History of How Our Government Segregated America (New York: W.W. Norton & Company, 2017). See “Mapping Inequality: Redlining in New Deal America” (2016), for a compilation of the maps and notes created by the federal Home Owners’ Loan Corporation in the 1930s that designated areas considered too risky for mortgage lending and were used to determine eligibility for Federal Housing Administration guarantees. Return to text

3. Lael Brainard, “Community Development in Baltimore and A Few Observations on Community Reinvestment Act Modernization,” (remarks delivered at the Federal Reserve Bank of Richmond Baltimore Community Development Gathering, Baltimore, Maryland, April 17, 2018). Return to text

4. In 2010, the three banking agencies held hearings on how to modernize the CRA regulations and subsequently issued revisions to the interagency guidance. In 2017, the agencies published additional findings on the CRA as part of the Federal Financial Institutions Examination Council 2017 Joint Report to Congress, Economic Growth and Regulatory Paperwork Reduction Act Review, March 2017. In 2018, the Office of the Comptroller of the Currency published an Advance Notice of Proposed Rulemaking (ANPR) asking for comments on a ratio-based approach to rating performance. The Federal Reserve reviewed the more than 1,500 comments on the ANPR and subsequently held about 30 outreach meetings with representatives of banks and community organizations, and the Federal Reserve Bank of Philadelphia hosted a research symposium. Return to text

5. Lael Brainard, “Community Investment in Denver,” (remarks delivered at the Federal Reserve Bank of Kansas City, Denver Branch, Denver, Colorado, October 15, 2018). Return to text

6. Lael Brainard, “Strengthening the Community Reinvestment Act: What Are We Learning?” (remarks delivered at the Research Symposium on the Community Reinvestment Act hosted by the Federal Reserve Bank of Philadelphia, Philadelphia, Pennsylvania, February 1, 2019). Return to text

7. Lael Brainard,”Keeping Community at the Heart of the Community Reinvestment Act,” (remarks delivered at the Association of Neighborhood and Housing Development Eighth Annual Community Development Conference Build.Community.Power, New York, New York, May 18, 2018). Return to text

8. The importance of constructing a consistent and comparable CRA database was a key theme at the Research Symposium on the Community Reinvestment Act hosted by the Federal Reserve Bank of Philadelphia on February 1, 2019. Return to text

9. In order for the retail lending metrics to provide a meaningful evaluation, a bank would also need to meet a minimum percentage of retail loans in its local community relative to its deposits. The bank’s ratio would be compared to a minimum activity threshold based on the performance of all reporting banks in that same assessment area, with the goal of screening out the lowest performers who would need to undergo a full review from an examiner. The minimum activity threshold would be calibrated for geographies and different market conditions over time. Return to text

10. Board of Governors of the Federal Reserve System, “Perspectives from Main Street: Bank Branch Access in Rural Communities,” (PDF) (Washington: Board of Governors, November 2019). Return to text

11. Lael Brainard, “The Community Reinvestment Act: How Can We Preserve What Works and Make it Better?,” remarks delivered at the 2019 Just Economy Conference, National Community Reinvestment Coalition, Washington, D.C., March 12, 2019. Return to text

12. Statewide activity outside of a bank’s local assessment area would factor into its statewide community development rating, and regional activities would be considered at the institution level. Return to text